The following is our summary of significant U.S. legal and regulatory developments during the second quarter of 2026 of interest to Canadian companies and their advisors.

FTC and DOJ Seek Public Comment on HSR Form and Scope of Longstanding Exemptions

On March 25, 2026, the Federal Trade Commission (the “FTC”) and the Department of Justice (the “DOJ”) Antitrust Division (together, the “Agencies”) issued a joint Request for Information (“RFI”) seeking public comment on the effectiveness of the revised Hart‑Scott‑Rodino (“HSR”) Premerger Notification and Report Form (the “2025 Form”), which was made effective on February 10, 2025, but vacated by a federal district court in February 2026. The Agencies are considering a new rulemaking to modify the vacated 2025 Form and potentially eliminate or reduce the scope of several longstanding HSR exemptions. Several items in the RFI stand out as having potentially significant consequences for non-US investors and parties engaged in real estate, defense and technology investments and minority acquisitions.

Key Takeaways

The RFI suggests that the Agencies are pursuing a two-track strategy in the next HSR rulemaking: seeking to reduce burdens for clearly non-problematic transactions while simultaneously expanding the reach of the HSR regime to capture a wider universe of transactions and more granular information. The RFI is intended to inform the Agencies’ consideration of a possible new rulemaking, which could take at least nine months to become effective.

Key RFI Proposals and Client Implications

-

Expanded Scope of the HSR Form: CFIUS, Foreign-Government, Sovereign Wealth Fund Disclosures

The Agencies are considering whether to require filers to disclose information regarding their compliance with the Committee on Foreign Investment in the United States (“CFIUS”) regime, including compliance with Section 721 of the Defense Production Act of 1950 and any CFIUS mitigation terms. The Agencies are also evaluating whether the current Form adequately captures the relationship between sovereign wealth funds and their affiliated sovereigns, and whether additional information should be required.

This proposal could effectively add a CFIUS and foreign investment compliance requirement onto the HSR process. For non-U.S. parties—including private equity sponsors backed by significant foreign limited partners, sovereign wealth funds and portfolio companies with foreign government-affiliated investors—this proposal could materially increase both the cost and complexity of HSR filings. Parties would potentially need to coordinate their CFIUS and HSR analyses simultaneously, and the HSR filing could become a vehicle through which the Agencies identify transactions that may warrant CFIUS review, including transactions that are subject to only voluntary CFIUS filing requirements.

-

Expanded Disclosures for Department of War Contracts

The Agencies are contemplating whether to require filers to disclose information about their contracts with, or direct and indirect sales to, the Department of War (the “DOW”), regardless of whether there is currently a horizontal competitive overlap between the merging firms. This represents a notable expansion of the vacated 2025 Form, which required DOW-related disclosures only where there was a horizontal overlap. For defense contractors and companies in adjacent supply chains, this proposal would increase disclosure burdens on all HSR-reportable deals regardless of the antitrust risks associated with the transactions.

-

Review of the Scope of the Investment-Only Exemption

The Agencies are considering whether to make explicit that the passive investor exemption “does not apply when the acquiror uses its ownership of voting securities to influence a corporation’s competitive decision-making, including the corporation’s policies that may affect prices, quality, or output.” The RFI also asks how often investors are “taking significant stakes in the same entity using different investment vehicles,” and what impact this has on effective premerger review.

The passive investor exemption is one of the most widely used exemptions in the investment community. This exemption allows investors to acquire a less than 10% stake in companies, without an HSR filing. For institutional investors, asset managers and private equity firms, any narrowing of this exemption could increase the number of HSR-reportable transactions, imposing substantial filing fees, legal costs and transaction timing delays on transactions that were previously exempt.

-

Closing the Gap on Non-Traditional Transaction Structures: Acquihires and Convertible Securities

The Agencies are evaluating whether to capture “non-traditional transaction structures” that are currently not reportable under the HSR Act but that “have the practical effect of eliminating a market participant.” Specific structures called out in the RFI include: (1) “acquihires” and “reverse acquihires,” including non-exclusive licensing agreements that leave the acquired entity intact but not competitively viable; and (2) purchase or sale of convertible securities that allow parties to consummate transactions meeting or exceeding reporting thresholds without triggering HSR filing obligations.

For technology companies, venture capital and private equity investors, and parties that frequently use convertible instruments (including convertible notes and Simple Agreements for Future Equity), this could result in a material increase in filing obligations, additional deal costs and greater scrutiny and timing delay of novel deal structures. Companies that have historically relied on the structuring flexibility of convertible instruments and talent acquisitions would need to reassess their transaction strategies.

-

Potential Elimination or Narrowing of Real Estate and REIT Exemptions

The RFI asks whether the longstanding real estate exemptions and REIT exemptions of the HSR rules should be removed entirely or re-evaluated. These exemptions have historically reflected the view that real estate acquisitions are “unlikely to violate the antitrust laws.” The Agencies now question whether this assumption remains valid, in part because of President Trump’s January 2026 executive order directing the Agencies to “review substantial acquisitions, including series of acquisitions, by large institutional investors of single-family homes in local single-family housing markets for anti-competitive effects.”

Removal of the real estate exemptions would have a sweeping impact on the real estate industry. Real estate funds, developers, institutional investors and REITs could face a dramatic increase in HSR-reportable transactions. For large institutional investors that engage in high-volume real estate acquisitions—particularly those purchasing single-family homes at scale—the cost and administrative burden could be substantial.

-

Structural Transaction Modifications and Late-Stage Remedies

The RFI raises the prospect of requiring new or supplemental HSR filings when parties propose structural modifications to a transaction—including divestitures or other remedies—during a Second Request investigation or after the Agencies have commenced enforcement litigation. The Agencies note that late-proposed remedies may “significantly alter the competitive analysis of the transaction as originally proposed” and that the Agencies currently lack “a mechanism for extending the waiting period in order to obtain documents and information sufficient to evaluate the altered transaction or divestiture.”

If adopted, this proposal would effectively create a new filing trigger for remedy proposals, potentially requiring parties to submit detailed information about divested and retained assets, standalone viability analyses, transition service arrangements and proposed divestiture buyers. This could significantly complicate and slow down the negotiation of consent decrees and fix-it-first remedies, and may discourage parties from proactively offering remedies to resolve agency concerns—an outcome the Agencies themselves acknowledge. Parties would also be required to pay additional HSR filing fees, which are currently as high as $2.46 million for transactions valued at or greater than $5.869 billion.

For the full text of our memorandum, please see:

For the Agencies’ joint RFI, please see:

FTC Seeks to Pause HSR Form Appeal Amid New Rulemaking Review

On May 18, 2026, the FTC filed an unopposed motion in the Fifth Circuit seeking to hold in abeyance, until the end of this year, its appeal of a district court order vacating the 2025 HSR Act notification requirements. On May 26, 2026, the Fifth Circuit granted the FTC’s motion. While the appeal is held in abeyance, the FTC is “seriously considering” potential new revisions to these 2025 HSR Act notification requirements. The FTC’s unopposed motion for abeyance follows the Eastern District of Texas’s February 2026 ruling invalidating the updated form and the Fifth Circuit’s subsequent denial of the FTC’s motion for a stay pending appeal on March 19, 2026.

Practically speaking, this motion for abeyance suggests the FTC’s new rulemaking expected later this year may ultimately moot or substantially narrow the scope of the appeal. The FTC’s appeal will remain technically alive but will be paused and unresolved. The FTC continues to accept HSR filings under the old, pre-2025 form.

Background: The HSR Act, the 2025 Form and Vacatur and the March RFI

-

HSR Act. The HSR Act requires parties to certain transactions exceeding specified monetary thresholds to file a premerger notification form with the FTC and the DOJ and observe a waiting period prior to closing.

-

2025 Form and Eventual Vacatur. In 2024, the FTC published a final rule substantially expanding the HSR premerger notification form and filing requirements. The changes took effect on February 10, 2025. The 2025 Form imposed a significantly greater burden and expense on filing parties. On February 12, 2026, in a challenge by the Chamber of Commerce to the FTC’s rulemaking, the Eastern District of Texas vacated the 2025 Form, and, on March 19, 2026, the Fifth Circuit denied the FTC’s motion for a stay pending appeal. As a result, the DOJ and FTC are currently accepting filings under the older, pre-2025 form.

-

RFI. As described above, on March 25, 2026, the DOJ and FTC published an RFI seeking public comment on potential improvements to the 2025 Form.

HSR filers will continue using the pre-2025 form for the foreseeable future and should maintain their current filing practices at least for the remainder of 2026. The FTC and DOJ will be reviewing public comments and likely will be developing a new proposed rule before the end of this year. This means filers face a prolonged period of uncertainty about what the eventual reporting requirements will look like—potentially stretching well into 2027 or beyond if a new rulemaking is initiated, since notice-and-comment rulemaking typically takes many months.

For the full text of our memorandum, please see:

For the full text of our previous memorandum concerning the Eastern District of Texas’s ruling vacating the 2025 Form, please see:

For the full text of our previous memorandum concerning the Fifth Circuit denying the FTC’s motion for a stay pending appeal on the Eastern District of Texas’s ruling vacating the 2025 Form, please see:

For the full text of our previous memorandum concerning the expanded 2025 Form, please see:

SEC Shortens Minimum Period for Certain Equity Tender Offers

The Securities and Exchange Commission (the “SEC”)’s Division of Corporation Finance has issued an exemptive order allowing certain equity tender offers to adopt a shortened 10-business day initial offering period (instead of the 20-business day period currently required). The relief applies only to fixed-price, cash tender offers that meet the following conditions. This will provide deal parties with additional flexibility in structuring transactions and may make two-step cash transactions more appealing in certain contexts given the potential speed to closing.

Conditions for Tender Offers for Equity Securities of Reporting Companies

-

The tender offer must be subject to the SEC’s tender offer rules under Regulation 14D or Rule 13e-4 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and not be a going-private transaction subject to Rule 13e-3 or a cross-border tender offer relying on exemptions under Rule 14d-1(d) or Rule 13e-4(i) of the Exchange Act;

-

There cannot be a previously announced or pending competing tender offer at the public announcement of an offer relying on this relief. If one is publicly announced after commencement, the initial tender offer period must be extended such that the offer is open for at least 20 business days from the date the initial offer commenced;

-

For third-party tender offers subject to Regulation 14D, (i) the offer must be for all outstanding securities of the subject class and be pursuant to a negotiated merger or similar business combination agreement between the subject company and the offeror and (ii) a Schedule 14D-9 must be filed and disseminated by the subject company no later than 5:30 p.m. Eastern time (ET), on the first business day after the tender offer’s commencement;

-

For issuer self-tenders subject to Rule 13e-4 under the Exchange Act, the offer must be for less than all outstanding securities of the subject class; and

-

The tender offer must be announced in a press release issued through a widely disseminated news or wire service by 10:00 a.m. ET on the commencement date of the tender offer. The press release must include the basic offer terms (such as the identity of the offeror, the class of equity security sought, the consideration offered and the expiration date of the offer) and an active hyperlink to a website where security holders may access the tender offer materials, letter of transmittal (if any) and any other documents related to the offer.

Conditions for Tender Offers for Equity Securities of Non-Reporting Companies

-

The tender offer must be made for the equity securities of an issuer that does not have a class of securities registered under Section 12 of the Exchange Act and is otherwise not subject to SEC reporting requirements under Section 15(d) of the Exchange Act; and

-

The tender offer must be made by the issuer of the securities sought in the tender offer or its wholly owned subsidiary.

-

In all cases, any (i) increase or decrease in the percentage of the subject securities sought in the tender offer (other than the acceptance for payment of an additional amount of securities not to exceed 2% of the subject securities) or (ii) change in the consideration offered, must be communicated no later than 9:00 a.m. ET on the fifth business day before expiration of the offer. Any other material change in the tender offer terms must be communicated by press release or other public announcement no later than 9:00 a.m. ET on the second business day before expiration of the offer. For tender offers for securities of reporting companies, these communications must be by press release or other widely disseminated public announcement. For tender offers for securities of non-reporting companies, securities holders must be noticed by appropriate methods. All tender offers remain subject to applicable federal securities anti-fraud and anti-manipulation laws and rules.

For the full text of our memorandum, please see:

For the SEC’s exemptive order, please see:

Second Circuit Affirms Dismissal of Section 11 Claim on Traceability Grounds

On March 24, 2026, in a per curiam opinion, the Second Circuit unanimously affirmed dismissal of a Section 11 claim brought by investors in securities issued by Barclays Bank PLC in a decision captioned Knapp v. Barclays PLC, No. 25-1631 (2d Cir. Mar. 24, 2026). Applying the Supreme Court’s decision in Slack Technologies, LLC v. Pirani, 598 U.S. 759 (2023), the Second Circuit held that Plaintiffs failed to plead that their specific securities—which were acquired through a reverse share split—could be traced to the purportedly misleading registration statement, requiring dismissal. This decision is consistent with other post-Slack decisions that have imposed strict tracing requirements in Section 11 cases at the pleading stage.

Background: Section 11’s Tracing Requirement and the Supreme Court’s Decision in Slack

Section 11 of the Securities Act of 1933, as amended (the “Securities Act”), imposes liability for material misrepresentations in registration statements. In Slack, the Supreme Court unanimously held that Section 11 “requires a plaintiff to plead and prove that he purchased shares traceable to the allegedly defective registration statement.” Since then, many courts have applied a strict tracing requirement to dismiss Section 11 claims at the pleading stage where plaintiffs failed to allege that the shares they purchased were issued pursuant to the registration statement they challenged. For instance:

-

In Slack, the Ninth Circuit on remand held that this pleading standard was not met because the company went public through a direct listing in which both registered and unregistered shares were immediately tradeable, and plaintiffs failed to show that the shares they acquired were registered.

-

In Shnayder Allbirds, Inc., No. 23-cv-01811-AMO (N.D. Cal. June 23, 2025), a district court in California reached a similar conclusion where a defendant went public through a typical IPO but where certain employees were permitted to sell preexisting unregistered shares during the first seven days of public trading.

-

In In re The Honest Company Securities Litigation, 21-cv-7405 (C.D. Cal. May 1, 2023), a district court significantly narrowed a certified class in a Section 11 case to include only investors who purchased shares before the end of the post-IPO 180-day “lock up” period, at which point unregistered shares could be traded in the market.

Although these decisions involved situations where registered and unregistered shares commingled in the markets, their reasoning implied that, when a company issues shares pursuant to multiple registration statements in multiple offerings, courts will dismiss a Section 11 complaint where plaintiffs fail to plead that their specific shares were issued pursuant to the specific offering documents they challenge.

The District Court’s Dismissal Decision in Knapp

Plaintiffs in Knapp were investors in exchange-traded notes (“ETNs”) issued by Barclays under the ticker VXX. On April 23, 2021, Barclays executed a 4:1 reverse split of VXX, where the issuer replaced every four ETNs held by investors with a single new ETN worth four times the value. Plaintiffs had acquired their ETNs prior to the reverse split, and their ETNs were exchanged in the reverse split. Also on April 23, 2021, Barclays filed a registration statement—called a “pricing supplement”—pursuant to which Barclays could sell post-split ETNs it held in inventory.

Plaintiffs sued under Section 11 and alleged that the pricing supplement was a new registration statement that incorporated materially misleading statements from earlier prospectuses. The district court dismissed the Section 11 claims because it determined that plaintiffs’ ETNs were not traceable to the allegedly defective registration statement (the pricing supplement, here). Plaintiffs appealed.

The Second Circuit Affirms Dismissal on Tracing Grounds

On March 24, 2026, Second Circuit Judges Walker, Sullivan and Bianco issued a unanimous, per curiam opinion affirming dismissal of the Section 11 claims. The court applied the Supreme Court’s ruling in Slack and explained that plaintiffs’ claims required them to plead that the securities offered in the pricing supplement “included the ETNs transferred to the Investors via the reverse split.” But the pricing supplement’s language made clear that it governed issuance only of ETNs “that Barclays still held in its inventory, and which it had thus not distributed via the split.” Accordingly, the investors “failed to plead any facts tracing their ETNs – which they acquired via the reverse split – to the” allegedly misleading pricing supplement.

Implications

The Knapp decision reinforces the strict traceability requirement the Supreme Court articulated in Slack and makes clear that Section 11 plaintiffs must do more than summarily plead some connection between a registration statement and their securities—rather, plaintiffs must plead specific facts demonstrating that their securities were offered pursuant to the precise registration statement they challenge. The decision joins a growing body of precedent in which courts, at the motion to dismiss stage, engage in a rigorous and technical analysis of offering documents and market realities to determine whether plaintiffs’ shares can be traced with certainty to the allegedly deficient offering they challenge. As more courts apply Slack and require plaintiffs to allege facts—and not mere conclusions—about the traceability of their shares, we may continue to see Section 11 claims dismissed where an issuer-defendant’s registered and unregistered shares, or shares issued pursuant to multiple registration statements, commingle in the market.

For the full text of our memorandum, please see:

For the Second Circuit’s decision in Knapp, please see:

For the full text of our previous memorandum concerning the Supreme Court’s decision in Slack, please see:

Ninth Circuit Affirms Dismissal on Loss Causation Grounds Based on Modest Size and Short Duration of Stock Drop

On February 6, 2026, a unanimous panel of the Ninth Circuit affirmed dismissal of securities fraud claims on loss causation grounds where the stock price decline following the purported revelation of the fraud was “modest, typical, and quickly reversed.” The decision in Nova Scotia Health Employees’ Pension Plan v. Comerica Inc., 2026 WL 323711 (9th Cir. Feb. 6, 2026), is the latest in a series of opinions in the Ninth Circuit to have applied a rigorous loss causation analysis at the pleading stage, and dismissed fraud claims as a matter of law, based on the size, typicality, and duration of the stock drop alone.

Background: Loss Causation

Loss causation is an essential element of a securities fraud claim under the Exchange Act. A variant of common law proximate causation, loss causation under the Exchange Act requires a plaintiff to demonstrate that a defendant’s misstatement, as opposed to some other fact, foreseeably caused the plaintiff’s loss. This typically requires an investor-plaintiff to identify a stock drop following the revelation of the defendant’s alleged fraud, which, the plaintiff argues, represents the amount by which the defendant’s fraud had artificially inflated its stock price. Unlike some other jurisdictions, the Ninth Circuit applies the heightened pleading standard of Rule 9(b) to loss causation and thus requires plaintiffs to plead with particularity the causal connection between the defendant’s misstatements and the plaintiff’s economic loss.

The Ninth Circuit Decision in Comerica

In Comerica, Plaintiffs alleged that defendants defrauded investors by concealing regulatory violations, and that an article published in May 2023 partially revealed the fraud—and satisfied loss causation—by reporting on defendants’ compliance violations, which purportedly drove a 7.4%, two-day stock drop. The district court held that the stock price movement following this article could not satisfy loss causation and granted defendants’ motion to dismiss.

On February 6, 2026, in an unpublished opinion, Ninth Circuit Judges Lee, Koh, and De Alba unanimously affirmed dismissal on loss causation because the stock price decline following the article “was modest, typical, and quickly reversed.” First, the court explained that the 7.4% decline was “smaller than the 10% drop that this court considered ‘modest’ in Metzler.” Second, the court noted that the decline was “well within Comerica’s typical stock price movement.” As the district court noted, the issuer’s stock price fluctuated by amounts greater than the stock drop on 12 of 43 trading days (28%) in the two months surrounding the alleged corrective disclosure date. Third, the issuer’s stock recovered “over the next two days” and then “remained higher than it had been before the . . . article was published” for approximately four months.

Implications

The Comerica decision is an important circuit-level addition to the growing trend of Ninth Circuit cases dismissing securities class actions premised on stock drops that are modest, typical, and short-lived. Defendants facing securities fraud complaints should carefully analyze their stock price movement surrounding any alleged corrective disclosure dates to assess whether to argue that the complaint fails to plead loss causation based on price movement alone. It remains to be seen whether the Ninth Circuit will adopt similar reasoning in a published opinion, or whether courts in other circuits will follow the Ninth Circuit’s lead and apply similar loss causation analyses at the pleading stage—but the line of reasoning adopted by the Comerica court is one that defendants in cases outside the Ninth Circuit have a good faith basis for pursuing.

For the full text of our memorandum, please see:

For the Ninth Circuit’s decision in Comerica, please see:

Second and Eleventh Circuits Reject Novel Attempt to Expand Strict Liability for Short-Swing Profits Premised on Corporate Buybacks

The Courts of Appeals for the Second and Eleventh Circuits have both rejected a novel theory of strict liability under Section 16(b) of the Exchange Act, which requires company insiders to disgorge trading profits from matched purchases and sales of company stock in a six-month window. The appeals stemmed from lawsuits brought by a single investor against controlling shareholders of five companies seeking to recover trading profits by matching shareholder stock sales with corporate repurchases pursuant to stock buyback programs. Both appellate courts overwhelmingly rejected this theory as inconsistent with the plain language of the statute, agency interpretation and principles of equity. These opinions are welcome news to controlling shareholders and corporate insiders seeking to transact in company stock, and reinforce courts’ reluctance to expand the “harsh result” of strict liability statutes.

Factual Background

Section 16(b) of the Exchange Act, 15 U.S.C. § 78p(b), is a strict liability statute designed to prevent company insiders from profiting on the basis of nonpublic information. The statute requires the “beneficial owner, director, or officer” of an “issuer” to disgorge to the issuer any profits realized from a paired purchase and sale of company stock within a six-month period, “irrespective of any intent[],” subject to certain exemptions.

Beginning in 2023, an investor named Andrew Roth brought a series of lawsuits pursuing a novel theory of Section 16(b) liability against the controlling shareholders of five different companies—Estée Lauder Companies Inc., Altice USA, Inc., Luminar Technologies, Inc., Hertz Global Holdings, Inc. and T-Mobile US, Inc. In each case, Roth argued that the controlling shareholders—“beneficial owners” under the statute—were required to disgorge millions of dollars in short-swing profits to the respective companies because, within six months of the controlling shareholders selling shares, the companies repurchased their own shares pursuant to stock buyback programs. Roth argued that these transactions—the shareholders’ sales and the companies’ repurchases—were matchable under Section 16(b) because the controlling shareholders had an indirect pecuniary interest in the issuer repurchases.

The federal district courts repeatedly rejected Roth’s theory and dismissed all five of Roth’s actions. The courts held, among other things, that the plain text of Section 16(b) treats “beneficial owners” and “issuers” as separate entities that necessarily cannot have matched transactions. Roth appealed four dismissals: the Second Circuit combined oral argument on two appeals and held a third appeal in abeyance pending the outcome of the two argued appeals. Another dismissal was appealed to the Eleventh Circuit.

The Second Circuit Opinion

In May 2025, the Second Circuit issued an opinion affirming the dismissal of Roth’s cases against the controlling shareholders of Estée Lauder and Altice. Judge Jacobs, writing for himself and Judge Nathan, explained that because the statute provided for the “harsh measure of strict liability”—which is “arbitrary, some might say Draconian”—Congress imposed “narrowly drawn limits on Section 16(b)’s scope.” The court held that plaintiff’s theory did not fit within these limits because it was incompatible with the “mechanical application” of matching purchases and sales under Section 16(b). The court elaborated on five ways in which plaintiff failed to state a claim:

First, the statute requires a defendant to have “beneficial ownership” in the shares in each matched transaction. But repurchased shares are instantly transformed into treasury shares, which are valueless and not shares in which a corporate insider can have a pecuniary interest. Second, and relatedly, matched transactions must involve substantively identical equity securities, but the controlling shareholder’s sold equity shares were different in kind from the repurchased treasury shares. Third, because the controlling shareholder lacked a pecuniary interest in the repurchased shares, it did not realize any profit, as required by the statute. Fourth, it would be inequitable to require the controlling shareholder to disgorge profits to the issuer based on the issuer’s decision to repurchase shares. Fifth, the court refused to impose strict liability on company insiders for corporate repurchases over which they may have no inside knowledge, and rejected plaintiff’s attempt to expand Section 16(b) strict liability “by invoking a policy argument to the contrary.”

Judge Calabresi wrote separately, concurring in the judgment and “not disagree[ing] with the majority’s analysis,” but noting his preference to decide the issues more “narrowly.”

Although Roth initially indicated his intent to pursue Supreme Court review, he did not file a petition for certiorari before the deadline, and the Second Circuit opinion is now final.

Following the Second Circuit’s opinion, Roth also stipulated to the dismissal, with prejudice, of his appeal from the dismissal of his substantially similar suit against the controlling shareholders of Hertz, which had been held in abeyance. Roth then sought to withdraw that stipulation, but on June 25, the Second Circuit denied that request and so-ordered the stipulation of dismissal.

The Eleventh Circuit Opinion

In June 2025, Judges Luck, Lagoa and Abudu of the Eleventh Circuit issued a unanimous, per curiam opinion also affirming the dismissal of Roth’s case against the controlling shareholder of Luminar Technologies. Like the Second Circuit, the Eleventh Circuit noted that it was inappropriate to impose strict liability “on the basis of unclear language” or without an “unmistakable reference.” The court held that the plain text of Section 16(b) did not apply to issuer repurchases of its own stock on the open market and that a controlling shareholder does not have a pecuniary interest in repurchased shares. The court also relied on an SEC rule that previously exempted stock repurchases from Section 16(b). Although that rule was repealed in 1991, this was done because, in the SEC’s view, “transactions by the issuer are not subject to Section 16 since the issuer is the beneficiary of the short-swing profit provision,” and therefore the exemption was unnecessary.

The deadline to seek Supreme Court review of the Eleventh Circuit’s opinion has also passed, and that decision is now final.

Implications

The decisions by the Second and Eleventh Circuits resoundingly reject Roth’s theory that a controlling shareholder sale can be matched against an issuer repurchase simply because these shareholders may have a pecuniary interest in the transactions of the company. These opinions should provide comfort to controlling shareholders—and company insiders more generally—who sell shares (or intend to sell shares) of company stock. More broadly, these opinions reinforce the principle that courts will narrowly interpret statutes, such as Section 16(b), that impose the “harsh result” of strict liability, and treat with skepticism “policy argument[s]” or other creative attempts to expand such liability. We will continue to monitor for further developments and provide updates if additional cases pursuing similar theories are filed.

For the full text of our memorandum, please see:

For the Court of Appeal for the Second Circuit’s opinion, please see:

For the Court of Appeal for the Eleventh Circuit’s opinion, please see:

Delaware’s First Read on the DGCL Section 144 Safe Harbor

Recently in Ayers v. Foley, the Delaware Court of Chancery issued an opinion (by Vice Chancellor Will) interpreting for the first time certain provisions in the 2025 amendments to Section 144 of the Delaware General Corporation Law (“DGCL”), the landmark statutory reforms that provide safe harbor protections for certain conflicted transactions. The practical takeaway of Ayers is that Section 144 has raised the bar materially for rebutting the presumption of director independence at the pleading stage for publicly listed corporations when the board has determined that a director satisfies the exchange’s independence requirements because of the statute’s “substantial and particularized facts” pleading requirement. Significantly, the court reached this conclusion in the context of determining the issue of demand futility, reasoning that the heightened pleading standard in Section 144 is not confined to the safe harbors in Section 144 and was intended to apply broadly to other contexts as well. Ayers also reaffirms that when directors approve their own compensation, they are necessarily interested and their actions continue to be subject to entire fairness review.

The dispute in Ayers concerned two decisions made by the compensation committee of the board of directors of Fidelity National Financial, Inc. (“FNF”) regarding: (a) annual non-employee director compensation over a three-year period and (b) a one-time equity grant (the “Equity Grant”) to the non-executive chairman (and founder). Given the significance of the Equity Grant, the compensation committee conditioned its approval on review and approval by an independent related person transaction committee, which approved the grant after reviewing market data from an independent compensation consultant. An FNF stockholder sued derivatively challenging the director compensation and the Equity Grant.

Key aspects of the court’s analysis concerning the statutory safe harbor include the following:

-

Section 144(d)(2)’s heightened presumption for director disinterestedness extends to—and therefore sets a new, higher pleading standard for—demand futility analyses. DGCL Section 144(d)(2) establishes a heightened presumption of disinterestedness to directors of listed corporations who are not a party to the challenged transaction and whom the board has determined to be independent under stock exchange rules. The court held that this presumption is not confined to the safe harbors set forth in Section 144 and applied it to its demand futility analysis relating to the Equity Grant. The court reasoned that the legislature limited other provisions of Section 144 to specific situations but included no such limiting language in paragraph (d)(2), reflecting an intent for the heightened presumption to apply broadly to contexts outside of Section 144.

The practical effect of the court’s conclusion is to raise materially the pleading standard for demand futility where the heightened presumption applies. In Ayers, the allegations of overlapping board service, minority sports-team co-investments and other business connections with the chairman were insufficient to show that a majority of the board lacked independence from the chairman so as to render demand futile under prong three of the demand futility analysis noted above.

-

Application of the safe harbor in Section 144(a)(1) and the corporation’s exculpatory charter provision means that a plaintiff must sufficiently plead bad faith to establish demand futility. Section 144(a)(1) provides that a conflicted director transaction may not be the subject of equitable relief, or give rise to an award of damages, against a director if it is approved, in good faith and without gross negligence, by the fully informed vote of a majority of the disinterested directors on the board or a board committee. The court reasoned that application of Section 144(a)(1)’s safe harbor combined with the Section 102(b)(7) exculpatory provision in FNF’s charter meant that the plaintiff must plead particularized facts indicative of bad faith to show that the directors faced a substantial threat of liability and thus that demand would be futile under prong two of the demand futility analysis noted above. In Ayers, the process related to the Equity Grant undercut the allegations of bad faith because the compensation committee relied on an outside compensation consultant, negotiated the award downward and conditioned its own approval on the separate review and approval of the related person transaction committee.

-

Director compensation decisions remain subject to entire fairness review absent disinterested stockholder approval. When directors approve their own pay, they are inherently interested. This can be cleansed by obtaining the approval of a majority of the votes cast by the corporation’s disinterested stockholders under the safe harbor in Section 144(a)(2). In Ayers, no disinterested stockholder approval was sought for the director compensation at issue. Defendants instead relied on the safe harbor in Section 144(a)(3), which insulates an interested director from liability if the transaction is fair to the corporation and its stockholders. This standard tracks the common law of entire fairness review that takes into account financial (fair price) and process (fair dealing) considerations in a unitary analysis. The court cited precedent holding that unfair dealing is effectively established at the pleading stage for self-compensation claims and held that unfair price had been adequately alleged based on evidence that the non-employee directors’ compensation outpaced peers even though the company lagged on certain market capitalization, revenue and net income metrics. The court then concluded that the breach of fiduciary duty claim survived against the compensation committee members who approved the director compensation awards but would be dismissed as to the directors who merely received compensation without participating in its approval, reasoning that they could not be liable absent allegations they knowingly accepted wrongful awards.

For the full text of our memorandum, please see:

For the Delaware Court of Chancery’s opinion in Ayers, please see:

SEC Proposes Overhaul of Securities Offering and Public Company Reporting Frameworks

The SEC is working hard to make good on Chairman Atkins’ promise to reduce the burdens and costs of going and staying public and facilitate access to the capital markets. On May 19, 2026, the SEC issued two proposals that would overhaul securities offerings and public company reporting. Together with the SEC’s recent proposal to permit semiannual reporting, its forthcoming proposals to reduce public company disclosure burdens and Chairman Atkins’ recent call for comments on how to modernize the IPO process, the public company landscape is undergoing a significant transformation.

The SEC’s securities offering proposal would substantially relax the requirements to be eligible to use Form S-3, widely extend the communications/registration benefits currently enjoyed by well-known seasoned issuers (“WKSIs”), permit forward and backward incorporation by reference on Form S-1, and adopt changes to the rules under the Securities Act to preempt state securities law registration and qualification requirements with respect to any offering registered under the Securities Act. The broad expansion would reduce the burdens of registered offerings for more issuers earlier in their public company life cycle.

The SEC’s public company filing status framework reform proposal would streamline and simplify the categories of domestic reporting issuers under the Exchange Act to just two: large accelerated filers and non-accelerated filers, and extend the disclosure scaling and reporting accommodations currently available to emerging growth companies and smaller reporting companies to all non-accelerated filers. The SEC rules would create a further subcategory of “small non-accelerated filers” for those issuers with less than $35 million in assets, which would be eligible for extended reporting deadlines. Non-accelerated filers would find their public company reporting burdens significantly reduced and all filers would benefit from the ease of navigating the streamlined framework.

In light of the work the SEC is separately undertaking with respect to foreign private issuers, the SEC has not at this time extended any of these proposed changes to foreign private issuers.

The comment period for the securities offering reform proposal will close on July 27, 2026, and the comment period for the public company filing status framework reform proposal will close on July 20, 2026.

Securities Offering Changes

Eligibility to Use Form S-3

The SEC’s proposal would focus Form S-3 eligibility on whether an issuer is current and timely in its public reporting. All other existing requirements for Form S-3 eligibility (including requiring one year of Exchange Act reporting history and a $75 million public float) would be eliminated. As a consequence, issuers could use Form S-3 immediately upon becoming subject to the reporting requirements of Section 13(a) or 15(d) of the Exchange Act, including for shelf offerings. To ensure investor protection in the expanded field of Form S-3 issuers, the SEC has proposed rules that would render certain issuers ineligible to use Form S-3.

Exchange Act reporting history: The SEC’s proposal would eliminate the requirement that issuers be subject to the reporting requirements of the Exchange Act for a period of 12 months. In line with the SEC’s focus on investors having access to all required information about an issuer, issuers would still need to be current and timely in their Exchange Act reporting for 12 months or such shorter period that they have been an Exchange Act reporting company to be eligible for Form S-3. The SEC has proposed a welcome grace period that would permit issuers to remain Form S-3 eligible notwithstanding an untimely filing, so long as the late filing was made within seven calendar days of its original due date (or the immediately following business day if the seventh calendar date is not a business day), and the issuer made only one untimely filing during the lookback period. Issuers relying on Rule 12b-25 would not have the benefit of an additional seven calendar days after the Rule 12b-25 deadline (but filings that comply with Rule 12b-25 would continue to be considered timely).

Other Form S-3 requirements: The proposal would otherwise delete Form S-3 requirements relating to:

-

certain failures to make payments and defaults;

-

all transaction requirements (including the requirement that issuers have a public float of at least $75 million and that offerings be for cash);

-

electronic filing and interactive data files; and

-

successor registrants (the SEC did note that successor registrants would not be tainted by tardy or delinquent filings by their predecessors and would only need to consider their own Exchange Act reporting history for the purpose of determining Form S-3 eligibility).

Form S-3 would continue to not be available for the registration of exchange offers and business combinations.

Ineligible issuers: In order to safeguard investors, the SEC’s proposal would prohibit certain issuers from using Form S-3, including issuers that are, or were in the past three years, blank check companies, shell companies (other than a business combination related shell company) and penny stock issuers, as well as issuers convicted of specified felonies or misdemeanors, or the subject of certain judicial or administrative orders or SEC proceedings. Notwithstanding the foregoing, former SPACs that are no longer shell companies would be eligible to use Form S-3.

Other prohibited issuers: Foreign governments, foreign private issuers, asset-backed issuers, investment companies and business development companies would be prohibited from using Form S-3.

Subsidiaries: Majority-owned subsidiaries that are not ineligible or otherwise prohibited as noted above, would continue to be eligible to use Form S-3 if their parent is eligible and if they are a co-registrant with their parent on the same registration statement, for the registration of fully and unconditionally guaranteed non-convertible securities (other than common equity).

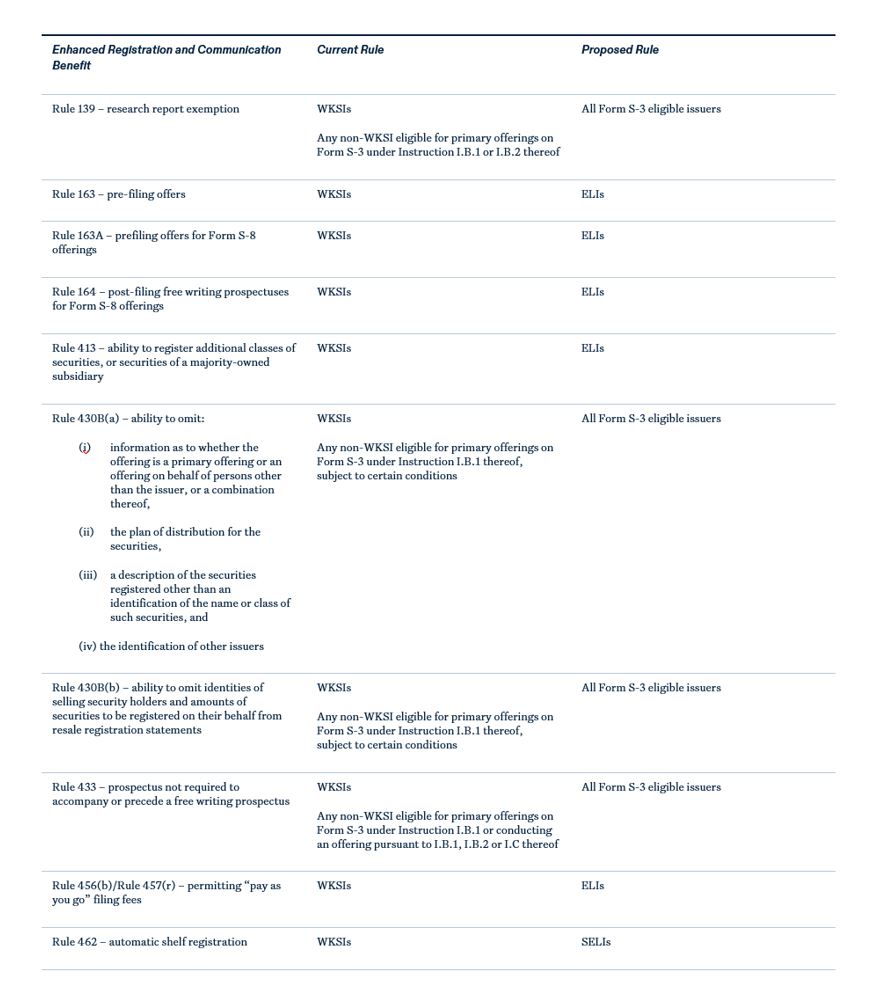

Enhanced Communication and Registration Benefits

The SEC has proposed eliminating WKSI status for domestic issuers and replacing it instead with two categories of issuers:

-

Eligible Listed Issuers (“ELIs”) – issuers eligible for Form S-3 who have a class of common equity securities listed on a national securities exchange; and

-

Seasoned Eligible Listed Issuers (“SELIs”) – ELIs who have been subject to the Exchange Act’s reporting requirements for a period of at least 12 full calendar months preceding the relevant measurement date. Successor issuers (other than former SPACs) would be able to rely on the Exchange Act reporting history of their predecessors for purposes of determining whether the successor satisfies the 12-calendar month seasoning requirement. Former SPACs would not be able to rely on their predecessor’s reporting history for the purposes of meeting SELI eligibility.

Neither ELI nor SELI status would retain a public float/registered debt issuance requirement, vastly expanding the issuer pool eligible to use these rules. In its proposing release, the SEC noted that in 2024, approximately 36% of Exchange Act reporting issuers were WKSIs; by contrast, 74% of Exchange Act reporting issuers in 2024 would have qualified as SELIs. The SEC would retain the WKSI definition for foreign private issuers, and is not proposing extending these amendments to foreign private issuers at this time. Like WKSI status, ELI and SELI status would be measured once a year.

ELIs would be eligible to use the enhanced communication and registration benefits currently afforded to WKSIs, except for automatically effective registration statements – only SELIs would be eligible to file automatically effective registration statements. Consistent with current rules which permit non-WKSIs eligible to use Form S-3 for primary offerings to use Rules 139 (research report exemption), 430B (permitting the omission of certain disclosure from the registration statement) and 433 (not requiring a prospectus to accompany or precede a free writing prospectus), Form S-3 eligible issuers would be eligible to rely on Rules 139, 430B and 433 as well. See below for a summary of the proposed changes.

|

Subsidiaries: Majority-owned subsidiaries using Form S-3 as described above would be eligible to be treated as an ELI or SELI, according to the status of the parent.

Incorporation by Reference on Form S-1

Those few issuers still using Form S-1 after the SEC’s proposed amendments become effective that are subject to, and have been current in their, Exchange Act reporting (though they need not have been timely) would be freely able to incorporate by reference into their registration statements on Form S-1, both backwards and forwards, their Exchange Act reports and any Securities Act registration statement filing (if no Form 10-K is yet filed). Issuers that are or were in the prior three years blank check companies, shell companies and penny stock issuers would not be eligible to incorporate by reference, nor would issuers registering an offering that effects a business combination on the Form S-1. Notwithstanding the foregoing, former SPACs would be eligible to incorporate by reference on Form S-1.

The categories of issuers ineligible to use Form S-1 would be expanded: currently foreign governments and asset-backed issuers are ineligible to use Form S-1; under the proposed rules, foreign private issuers, investment companies and business development companies would also be ineligible.

At the Market Offerings

In light of the expanded access to Form S-3 and shelf offerings, the SEC has proposed amending Securities Act Rule 415(a)(4) to restrict at-the-market offerings to just those securities that are listed or traded only on a national securities exchange, or in a market designated by the SEC (currently, Rule 415(a)(4) only requires that the securities be sold into “an existing trading market” for the outstanding securities).

Pre-emption of State Securities Laws

To reduce the burdens of blue sky compliance and facilitate capital formation, the SEC has proposed technical amendments to Securities Act rules that would exempt all securities offerings under Securities Act registration statements from state securities laws.

Public Company Filing Status and Reporting Changes

The many efforts the SEC and Congress have undertaken over the last quarter century to reduce burdens for various issuers to access the public markets and reduce reporting burdens have resulted in several complicated sets of sometimes overlapping filing statuses and varied reporting obligations. The SEC has proposed simplifying this framework and extending the scaled disclosure and reporting requirements to reduce regulatory burdens and encourage more companies to go and stay public.

Large Accelerated Filers

Under the SEC’s proposal, issuers that meet the following public float and reporting history requirements would be considered large accelerated filers:

Public float: A public float held by non-affiliates of $2 billion (up from the current $700 million), calculated based on the average stock price over the last 10 trading days of the second fiscal quarter, or first six-month fiscal period if semiannual reporting is adopted (extended from the current measurement of market capitalization as of the last day of the second fiscal quarter, to mitigate the impact of a single trading day’s volatility on the determination), in each of the last two fiscal years (up from just the most recent fiscal year, to ensure relative stability of the issuer’s status, as well as to provide early visibility into the possibility of a status transition). Because of the heightened thresholds to be met, the SEC has proposed the same standard for measuring both when an issuer would become a large accelerated filer as well as when an issuer would lose its status as such.

Public reporting: 60 consecutive calendar months of reporting (up from a year to allow companies additional time to adjust to being public before needing to comply with the full complement of requirements applicable to large accelerated filers). The SEC has requested comment on whether it would be appropriate to shorten this period for especially large public companies for whom the burden of public reporting as a large accelerated filer should be mitigated by their resources.

According to the SEC’s estimates, 19.2% of existing Exchange Act reporting companies would be large accelerated filers under the proposed rules, representing approximately 93.5% of total market public float.

The filing obligations of large accelerated filers would be unchanged.

Non-accelerated Filers

All issuers that are not large accelerated filers would be non-accelerated filers, eligible for the following scaled disclosure/reporting accommodations:

-

extended deadlines for periodic report filings (90 days for Annual Reports on Form 10-K; 45 days for Quarterly Reports on Form 10-Q);

-

no need to provide an auditor attestation report pursuant to Item 308(b) of Regulation S-K;

-

prepare financial statements in accordance with Article 8 of Regulation S-X, including the reduced financial statement requirements thereof:

-

two years of audited statements of comprehensive income, cash flows and changes in stockholders’ equity (instead of three);

-

more condensed format for interim financial statements, financial statements for businesses and real estate operations acquired or to be acquired and pro forma financial statements;

-

-

reduced description of business (notably, segment disclosure would not be required and human capital resources disclosure would be limited to the number of employees) per Item 101(a) of Regulation S-K;

-

two years of MD&A (instead of three) per Item 303 of Regulation S-K;

-

reduced executive compensation disclosures:

-

two years of summary compensation table information (instead of three) per Item 402 of Regulation S-K;

-

executive compensation disclosures regarding three named executive officers (instead of five) per Item 402 of Regulation S-K;

-

no need to provide: compensation discussion and analysis, compensation policies and practices related to risk management, pay ratio disclosure, pay vs performance disclosure and specific executive compensation disclosure tables (grants of plan-based awards, pension benefits, option exercises and stock vested table and nonqualified deferred compensation) pursuant to Item 402 of Regulation S-K, or compensation committee interlocks and insider participation disclosure or Compensation Committee Report disclosure pursuant to Item 407 of Regulation S-K;

-

-

no need to hold “say on pay,” “say on frequency of pay” or “say on golden parachute” votes;

-

no need to provide:

-

risk factor disclosure in Forms 10-K and 10-Q (though issuers may find good reason to continue this practice and risk factor disclosure remains a registration statement requirement);

-

performance graph disclosure comparing stock performance to peers per Item 201(e) of Regulation S-K;

-

supplementary financial information reflecting retrospective material changes to the financial statements pursuant to Item 302(a) of Regulation S-K;

-

quantitative and qualitative disclosures about market risk pursuant to Item 305 of Regulation S-K;

-

policies and procedures for the review, approval or ratification of related party transactions per Item 404(b) of Regulation S-K;

-

audit committee financial expert disclosure in the first annual report;

-

certain payments made by resource extraction issuers pursuant to Rule 13q-1 under the Exchange Act.

-

Foreign Private Issuers and SPACs

As noted above, the SEC has deliberately excluded foreign private issuers from these proposed offering and filer status rule changes. Under the proposed rules, foreign private issuers would be ineligible to use Forms S-3 and S-1 (and thus could not take advantage of the offering reforms by filing on domestic forms instead of Forms F-3 and F-1), and would be ineligible for the expansion of the scaled disclosure requirements and reporting accommodations available to non-accelerated filers.

While shell companies would not enjoy the benefits of the securities offering reforms, as noted above, the SEC has very specifically provided that former SPACs would be eligible to do so.

Conclusion

Together, these proposed rule changes would vastly reduce reporting and registration burdens for many public companies, especially newly public companies. If the rules are adopted as proposed, upon completing its IPO, an issuer would have significantly reduced reporting obligations for the first five years, and the benefit of certainty about its reporting obligations for that five-year period. At the same time, that newly public issuer would have immediate access to Form S-3 (including incorporation by reference and shelf offerings) and the benefits of enhanced communications currently accessible only by WKSIs, and, after a year of timely reporting, access to automatic shelf registration statements, all of which would greatly facilitate access to capital markets. For companies debating the costs of going or staying public, these reforms could be very persuasive.

For the full text of our memorandum, please see:

For the SEC’s securities offering proposal, please see:

For the SEC’s public company filing status framework reform proposal, please see:

SEC Proposes Semiannual Reporting Option

On May 5, 2026, the SEC issued its much-anticipated proposal to permit issuers subject to Sections 13(a) or 15(d) of the Exchange Act to report on a semiannual basis on a new Form 10-S instead of on a quarterly basis on existing Form 10-Q. New Form 10-S would have the same disclosure requirements as existing Form 10-Q, except over a fiscal six-month period instead of a fiscal quarter. This proposal follows President Trump’s advocacy of the issue last fall and during his prior administration. In its proposing release, the SEC noted its hope that this flexibility in choosing reporting cycles could reduce the burdens of being a public company and might prove influential in companies’ decisions to become or remain public companies.

Under the proposal, issuers would make an annual election regarding reporting by checking a box on the cover of their Annual Report on Form 10-K (or, if they are in the process of going public, by checking a box on the cover of their registration statement under the Securities Act). Issuers filing semiannually on Form 10-S would have the same length of time to file the Form 10-S as Form 10-Q, with the Form 10-S due 40 days (for large accelerated and accelerated filers) or 45 days (for all other filers) after the end of the first semiannual period of the fiscal year.

While the proposed rules seek to ease the significant reporting burdens on U.S. public companies, they also come at a time where shareholder engagement has become more muted and opaque. Active long investors are clamoring for access to management teams year-round and the unprecedented capital demands brought on by AI have made many companies more reliant on the debt capital markets than ever before.

Investor expectations and market forces favoring continued quarterly reporting will be significant, and in most cases, an outcome-determinative factor, for companies weighing the adoption of semiannual reporting. We outline some key considerations below:

Meeting Market Information Demands

For most public companies, investors will continue to expect a regular cadence of investor communications that extends beyond semiannual disclosures. Investor information demands may increase when a company is planning or executing significant transactions, undergoing strategic or operational transformation, navigating leadership transitions or experiencing material changes to its business. The fact that a company reduces the frequency of its public disclosures is unlikely to stem investor inbounds. Instead, a lack of information would in most cases likely create friction between a company and its investors, lead investors to assume the worst and result in a “going dark” discount being applied to the stock.

Sell-side analysts and credit rating agencies also rely on public disclosures to inform their price targets, ratings and recommendations. Keeping analysts and credit rating agencies apprised of material developments can help ensure the company remains visible to the right investors, avoid stale or inaccurate coverage, and mitigate the risk of unwarranted rating pressure or wider credit spreads.

Maintaining Investor Credibility

Credibility with investors is difficult to build and can be easily lost. Companies win credibility with investors by consistently providing clear information, communicating predictably, and delivering on targets and guidance. A regular cadence of investor communications is a key tool for building credibility: earnings calls, investor presentations, and investor days help shape the market’s understanding of the company’s narrative and reinforce confidence in management. Consistent, well-articulated messaging—especially around strategy, risks and performance drivers—reinforces trust, while opaque or stale narratives can quickly undermine it.

The loss of investor credibility can have significant adverse consequences: many activist campaigns trace their origins to investors who have lost faith in management and become more receptive to the ideas and demands of activists. For companies that have already built significant credibility with their investor base, there may be some limited flexibility to pare back disclosures. But going completely silent with financial disclosures between semiannual reports will disappoint investors at even the most well-respected companies.

Retaining Control Over the Strategic Narrative

Silence creates a narrative vacuum. This can be particularly dangerous for companies that are vulnerable to shareholder activism. Whether an activist succeeds often depends on its ability to craft a compelling narrative of repeated missteps, leaving investors with little choice but to support the activist’s demands. These narratives typically begin in private conversations among activists and other investors. When companies forgo public disclosures, they may also forgo opportunities to correct or reshape what is being said behind closed doors. By the time an activist goes public, the company’s response may be at best reactive and potentially too late. In addition, a company that moves to semiannual reporting will be subject to an activist attack on this basis alone, and activists calling for a company to switch back to quarterly reporting could potentially obtain significant support from investors.

Ensuring Effective Shareholder Engagement

When done effectively, shareholder engagement can help companies identify and proactively address investor concerns and build a trusted line of communication. But federal securities laws and investor policies limit what can and cannot be said during engagement meetings. Regulation FD prohibits the selective disclosure of material non-public information. In addition, the SEC’s recent guidance on Schedule 13G filing eligibility has led to more muted engagement from the largest passive investors. Going forward, companies will need to continue to ensure the timely disclosure of material non-public information so it can be addressed in investor engagement meetings.

Navigating Compliance Challenges

The proposed semiannual reporting regime would operate within a broader regulatory, contractual and market framework that assumes the availability of quarterly financial statements. Consequently, semiannual reporting would introduce significant operational and governance complexities. A key practical challenge arising from semiannual reporting is its impact on trading windows. Companies in possession of quarterly financial information that is not publicly disclosed will need to impose substantially longer blackout periods on the ability of directors, officers and employees to trade; limit or delay share repurchases; and face greater constraints in accessing the capital markets.

Managing insider trading and Regulation FD compliance risk and establishing protocols for investor meetings and communications would also become more complex for companies that decide to adopt semiannual reporting. Such companies will need to make more judgment calls on when and how material nonpublic information gets released to the market. Semiannual reporting could also conflict with contractual disclosure obligations under credit and debt instruments that often require quarterly financial information. Attention may also need to be given to compliance with national exchange and accounting rules to the extent they are not revised to align with the shift to semiannual reporting.

While the SEC’s proposed semiannual reporting rules intend to provide companies with greater flexibility in reporting their financial results, widespread adoption appears unlikely. Investor information demands coupled with the practical realities of managing shareholder engagement, activism risk, capital markets access and compliance obligations, will in most cases continue to make quarterly reporting standard practice among established public companies.

For the full text of our memoranda, please see:

For the SEC’s proposal, please see:

* * *